Electricity is the lifeblood of modern economies. When the power supply falters or prices skyrocket, industries are held hostage, productivity lags, and development suffers. Evidence from around the world shows just how damaging unreliable or expensive energy can be for firm performance and investment. Yet in many developing countries, a curtain of secrecy shrouds the power sector. Contracts that determine how electricity is bought, sold, and priced often remain hidden, making it nearly impossible to detect whether high tariffs are driven by real market fundamentals—such as high risk and genuine cost structures—or by more nefarious reasons, such as rent extraction.

In ongoing work, we are peeling back that curtain. It is a testament to Pakistan’s commitment to transparency that NEPRA, the public regulator, posts contract details online. We collect detailed information on all power contracts in the country—including how they allocate risk, structure costs, and reward developers—we are piecing together our argument that “lopsided” contracts are enabling power producers to capture extraordinary returns at the expense of consumers and the broader economy. We compare these findings with neighbouring markets with somewhat similar risks but more competition. Our data reveal stark concerns of potential rent extraction in Pakistan’s power sector.

This article summarizes our key findings and places them in broader context. The story of Pakistan’s power sector may have echoes in other weakly regulated environments, such as public works procurement, where big-ticket contracts can be used to drum up returns under the facade of legitimate risk coverage.

Pakistan’s Power Landscape

Pakistan’s power sector serves nearly 200 million people. Three-fifths of electricity generation comes from fossil fuels, one-fifth from hydropower, and the remaining is mostly nuclear with a small proportion of solar, wind, and biofuels. There is not much of a market, at least not yet: a single government-backed entity buys all electricity. A little less than half of all electricity generation is through independent power producers (IPPs). A spot or wholesale market for electricity is in the works.

In the mid-1990s, against the backdrop of supply shortages, the government allowed private entry into electricity generation though the signing of long-term power purchase agreements (PPAs). Given substantial political volatility, to attract IPPs the government offered contracts that provided insulation against various risks – economic, political, and financial – by providing hedges, sovereign guarantees and reimbursement for any increase in costs. The tariff within these PPAs covered both fixed and variable costs. The fixed component, called the capacity purchase price, comprises of project debt payments, return on equity, equipment and insurance. The variable component, called the energy purchase price, consists of the fuel cost and operation/maintenance costs.

Why Contracts Matter More Than You Think

Electricity is often referred to as “the backbone” of the economy, but that backbone is only as strong as the contracts and incentives that underpin power generation and distribution. In a well-functioning market, investors require a fair return on capital and assurance that payments are made, while governments seek to procure stable power at the lowest cost for the public. In principle, long-term power purchase agreements (PPAs) can promote investment by guaranteeing that, once a power plant is built, the developer has a buyer for the electricity generated.

However, the real devil lies in the details of these PPAs. Does the government fulfil its financial obligations on time? Do PPAs lock in exorbitant returns for private producers? Who bears the risk of exchange rate fluctuations? How are cost overruns handled, especially in volatile contexts where fuel prices or equipment costs can spike unexpectedly? Answering these questions transparently can mean the difference between having fairly priced electricity and an economic albatross.

Mapping the Full Universe of Pakistan’s PPAs

To quantify the scale and significance of these arrangements, we assembled a dataset that spans every private power contract in Pakistan. Such data are usually off-limits because PPAs are confidential. Yet in Pakistan, the law requires NEPRA to disclose these contracts and their amendments over hundreds of separate documents.

Each PPA can be dozens of pages long, with many having multiple amendments which tweak the tariff, risk-sharing clauses, or key contractual definitions. Automating this process proved difficult. We thus scoured each contract line by line, recording how capacity payments, generation tariffs, return on equity, exchange rate indexation, and other key variables evolve over the contract’s typical 25- to 30-year duration.

We next extracted ownership details using publicly available records —who holds equity stakes, which individuals sit on company boards, and whether they have direct ties to influential groups. We are also tracking any histories of legal issues: criminal records, corruption probes, or court cases naming the developer.

Describing Pakistan’s Power Generation Contracts

Four facts characterise private PPAs in Pakistan:

- They were negotiated and signed bilaterally, without competitive procurement

- A long contract tenor, typically 25-40 years

- Cost-plus nature, with guaranteed real returns on equity often exceeding 20-25%

- Take-or-pay, meaning payments flow to generators irrespective of how much electricity they produce

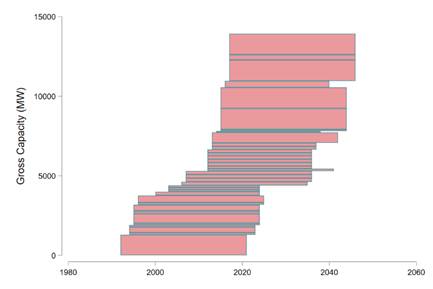

Figure 1: Gross Capacity Additions by IPPs in Pakistan’s Power Sector

Figure 1 documents the size and length of each PPA in Pakistan. Two striking facts emerge. First, PPAs span decades. Second, more than half of contracted independent power generation came in following the introduction of the 2015 Power Policy. Introduced at a time of severe electricity outages, the government introduced a system of fast-tracking investments into the power sector. Coupled with large external financing from China under the China Pakistan Economic Corridor (CPEC), this resulted in a vast inflow of power generation capacity. Unfortunately, these capacity additions – now locked in well until the late 2030s and early 2040s – vastly exceeded electricity demand, which turned out to be much lower than originally estimated because of the economic slowdown and sharp reduction in the cost-alternative sources of power, particularly solar. This has resulted in a growing fiscal burden on the state.

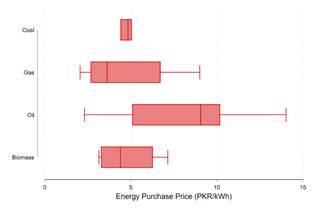

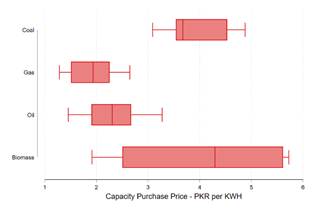

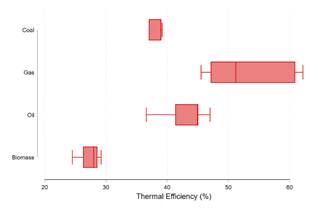

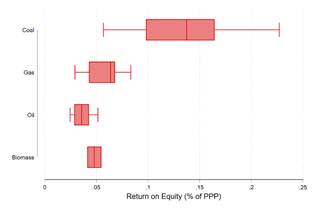

Figure 2: (Top-to-Bottom) Energy Purchase Price (EPP); Capacity Purchase Price (CPP); Thermal Efficiency; RoE.

Figure 2 characterises some of the key features of signed PPAs in Pakistan by fuel type. Naturally, fuels like gas or oil have larger energy costs compared to coal. Pakistan’s coal fleet, however, is characterised by comparatively large capacity costs, part of which is driven by a disproportionately higher return on equity as a share of the overall power purchase price (PPP). A large range of thermal efficiencies characteristic oil and gas plants – partially reflecting that these technologies have been in Pakistan’s electricity mix for far longer.

The Risk-Rent Connection

Our research zeroes in on the risk-hedging provisions and cost-plus nature embedded in power contracts. Recall that a cost-plus contract means that a power producer earns a given return above any costs they experience. On paper, these are meant to compensate developers for uncertainties: changes in currency value, debt costs, inflation, and commodity price shifts (e.g. coal). Yet in practice, if not carefully audited, these “risk cushions” can be used to extract rents. If regulators or procurement authorities are weak—or influenced by vested interests—contractual elements may be inserted that allow developers to pass almost all risks and cost increases to the government. Such a system also allows producers to get away with reported inflated costs or dialling down stated thermal efficiency rates to raise overall profits. Ratepayers then shoulder these burdens through higher electricity bills, whether or not the developers’ underlying costs truly justify it.

Not Everything is Quite as it Seems

Leaked evidence supports the above concerns. Past internal government analyses[1] document how IPPs are earning vastly more than contracted. Recorded profits are 83% higher on average than what they should have been as per the contract terms. Across the lifecycle of these plants, this amounts to a total of just over PKR 200 billion, more than double the annual federal budget for education. Converting these figures to annual real returns on equity, IPPs realized average returns of just over 37.4% compared to contracted average returns of 20.2%. Several of these PPAs were terminated or heavily adjusted by the government in October 2024.

Challenging the Standard Contract Model

We classify these contracts as “lopsided” because the rents, or gains, are disproportionately skewed towards IPPs. Classical contract theory frames an “efficient contract” as maximizing one party’s utility subject to the other’s reservation utility. This approach often remains silent on which agent’s utility should be prioritized—so long as the overall bargaining solution is feasible. Our evidence from Pakistan, however, reveals that maximizing the developer’s utility has serious knock-on effects across the entire economy. Excess returns in the power sector sap public resources, worsen debt, and degrade firm competitiveness. In short, these deals do not merely affect the contracting parties; they affect millions of electricity consumers and thousands of businesses in other sectors.

We also confirm that cost-plus contracts breed moral hazard. If developers know they can inflate costs—because any additional expense is simply passed on—they face minimal incentives to maintain efficiency. The result can be “within contract lying,” such as indexing to the U.S. dollar for components not actually imported. We argue that while some level of cost-plus contracting can be justified if risk truly is high, in Pakistan it likely goes far beyond that point, leaving the government paying for “phantom” costs that may never have existed.

The Bottom Line: Lopsided Contracts and the Economy

What are the economic implications of these contracts? High electricity prices reduce firm profitability, chill investment, and can push smaller enterprises out of business altogether. Higher prices slice off demand, further exacerbating capacity payment issues. From a macroeconomic perspective, Pakistan’s power sector woes contribute to a ballooning public debt and put pressure on currency reserves. Since many contracts are indexed to the U.S. dollar, exchange rate movements can cost the government billions. In some cases, foreign investors exploit this structure by offshoring profits or effectively hedging all exchange rate risks at the government’s expense.

Finally, the notion of allocative efficiency goes out the window. When electricity is artificially expensive, resources flow away from sectors that could use them productively. Firms that cannot afford high tariffs may scale back operations, reduce hiring, or exit altogether, while less efficient incumbents with enough capital to weather expensive electricity remain.

Takeaways

Where does this tale leave us? Four immediate policy ideas stem for this ongoing work.

#1: Implement competitive procurement. The single most direct way to rein in lopsided contracts is to force public auctions—where multiple bidders, including foreign developers, compete for the right to build and operate a power plant. This can dramatically reduce the scope for cozy behind-the-scenes deals, though we acknowledge that in weak institutional contexts, “auction design” can itself be manipulated.

#2: Improve disclosure requirements. Even if comprehensive auctions are not immediately viable, a more transparent and accessible publication of existing contracts (including all amendments) can help civil society, researchers, and the media shine a spotlight on abusive terms.

#3: Rebalance risk-sharing. Today, Pakistani IPPs pass virtually all cost overruns and exchange rate burdens onto the government. Why not a proportion, e.g. 50-50? Moving to partial or more balanced risk-sharing can reduce moral hazard. Of course, if government credibility is low, developers do need certain guarantees. But the pendulum has swung so far in favour of IPPs that it has created perverse incentives to inflate costs.

#4: Extend the scope of audits and regulatory bodies. In many countries, audits of procurement often focus on “hard” corruption (e.g., bribes, fake invoices) rather than scrutinizing the fairness or feasibility of contract clauses. This includes regular audits on thermal efficiency and other important power plant features. Regulators and courts should expand oversight to examine whether the contractual structure itself is beneficial or detrimental to the public good.

Towards a Fairer, More Efficient Power Sector

The tale of Pakistan’s electricity contracts underscores the dangers of unchecked power in procurement—quite literally. While risk is an inescapable reality in large-scale infrastructure, especially in Pakistan’s context with its legacy of delayed payments, it must still be priced sensibly, not exploited.

Yet this need not be a permanent state of affairs. With institutional strengthening—ranging from better disclosure to mandatory competitive bidding—it is possible to open up the “black box” of power procurement. By recalibrating contracts to share risk more equitably, the government can attract genuine investment while protecting public interests.

In the meantime, our findings also serve as a broader warning. Pakistan’s experience resonates with other countries where big projects are awarded with limited transparency. The lesson for policymakers is that rent extraction can come in obvious forms but also in more insidious, “legal” variants, like systematically lopsided contracts. Making these contracts public, quantifying their effects, and revealing who wins and who loses can be a critical first step toward genuine reform. Sunlight may indeed be the best disinfectant.

[1] Most notably, a March 2020 report by the Committee for Power Sector Audit, Circular Debt Resolution, and Future Roadmap led by Muhammad Ali.