Pakistan’s fiscal debate often sounds like a lament: revenue is low, deficits are chronic, and public services limp along. Yet the more striking fact is not how little Pakistan collects—but how predictably it fails to collect. The country has built a tax system that can count citizens, label them as filers, and withhold at the point of transaction—while remaining strangely incapable of taxing the powerful, rewarding growth, or renewing the bargain between state and society.

The result is a government that borrows to function and taxes in ways that punish formal activity and spare entrenched privilege. In 2023–24, nearly 79% of total tax revenue was consumed by interest payments—a statistic that should end most conversations about “fiscal space” before they begin.

Pakistan does not merely need “more taxes”. It needs a different logic: a tax system designed to enable development—grounded in evidence, tested in pilots, and scaled only when it works. In short, Pakistan needs to treat tax reform like applied science.

The anatomy of taxation

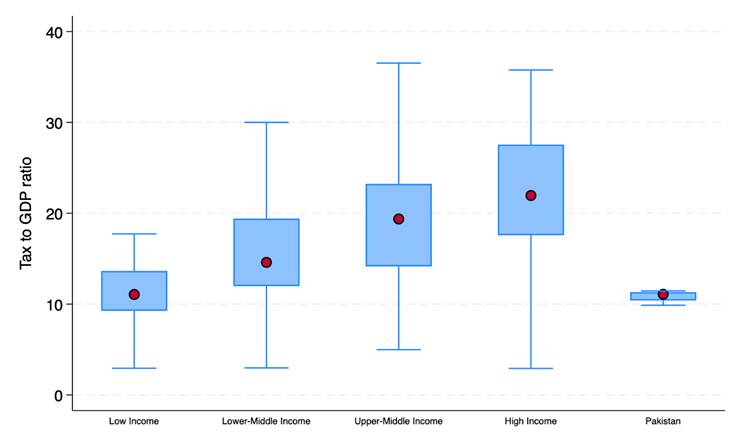

Start with the headline comparison. Pakistan’s tax-to-GDP ratio sits far below that of countries at similar income levels (Figure 1).

Figure 1: Pakistan collects far less tax revenue (as a share of GDP) than peer income groups. Data Source: UNU-WIDER Government Revenue Dataset (GRD 2023), averages for post-2015 years. Boxes show the middle 50% of countries in each income group (25th–75th percentiles); whiskers show the broader spread, and the dot is the group average.

Federal taxes flow through the NFC Award: 57.5% goes to provinces, and 42.5% remains with the federation. The provincial share is then distributed largely by population (82%), with additional weights for poverty/backwardness (10.3%), revenue generation (5%), and inverse population density (2.7%). This architecture matters because it shapes incentives. Federal dominance discourages provincial experimentation; local governments—often delayed or weakened—collect little themselves. Pakistan is formally a three-tier federation; fiscally, it operates as a one-tier system, with a fragile second tier and a non-existent third rung.

When you look at a province—Punjab, for instance—the pattern becomes visible (Figure 2): total revenues are dominated by federal transfers; own-source revenues are smaller; local revenues are smaller still. A state that cannot finance itself locally struggles to convince citizens that paying locally will yield local improvements. Trust does not thrive in abstraction.

Figure 2: Punjab Provincial and Local Revenues (FY2022–23, PKR billions). Data Source: Finance Department, Government of Punjab.

The myth of the “informal economy” as the main culprit

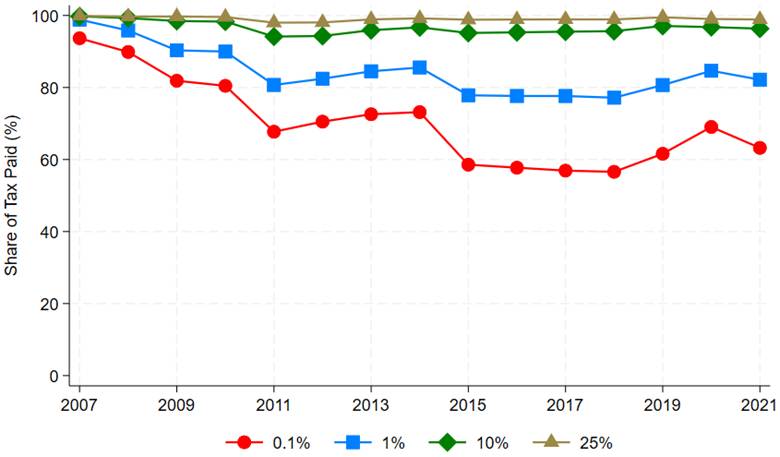

Pakistan’s tax discourse routinely blames “the informal economy,” often with a moral edge: too many people outside the net. But the data offer a less satisfying story—one in which poverty, not evasiveness, explains much of the missing base. According to Pakistan’s PSLM 2019 survey, more than 90% of working adults earn below PKR 600,000 per year, a threshold below which they are not required to report income to the FBR. In other words, only a small slice of adults are even supposed to pay income tax conventionally. And among those who do file, revenue is extraordinarily concentrated: about 80% of income-tax revenue is paid by 1% of filers, and about 60% by the top 0.1%.

Figure 3: Who actually pays? The extreme concentration of income-tax revenue. Source: Farooq, Rehman, and Waseem (2024)

This is not an argument for fatalism but for focus. A tax authority that spends political capital and administrative time chasing the wrong base ends up with a system that is busy, intrusive, and weak.

The “filing obsession”: counting people instead of collecting revenue

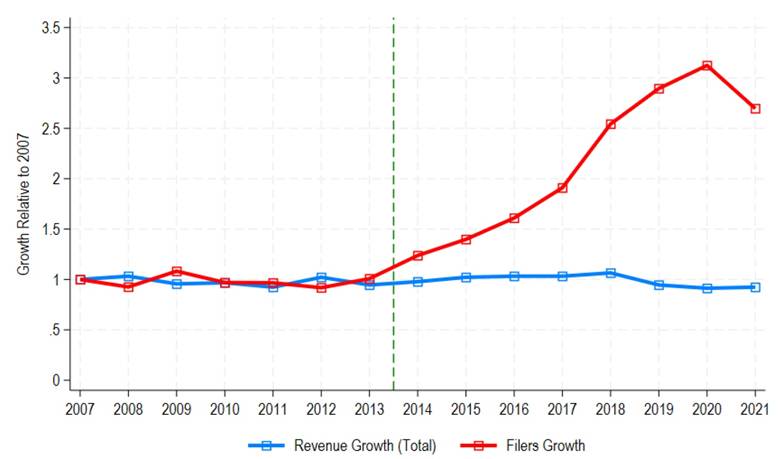

Pakistan has developed what can only be called a bureaucratic fixation with filing. Policies meant to penalize “non-filers” have produced an eightfold increase in filers since 2007, but this impressive statistic conceals a failure: the surge in filing has coincided with declining revenue as a share of GDP. In 2023, over 68% of returns filed were nil—a mass exercise in paperwork that strains administrative capacity without expanding fiscal capacity.

Figure 4: More filers, not more revenue. Filing expanded; revenue did not. Pakistan has become adept at producing “junk filers”. Source: Waseem (2024 presentation), using FBR Yearbook 2022–23

The deeper cost of this obsession is not merely administrative. It distorts behavior through high withholding and transaction restrictions, nudging firms and households to stay informal to avoid harassment. It also diverts attention away from high-value evasion—the only place where serious money (and serious fairness) resides.

Distortionary taxation: how the state taxes growth out of the economy

When enforcement is weak, governments reach for taxes that are hard to escape—even when those taxes are economically damaging. Pakistan relies heavily on turnover taxes, withholding taxes on transactions (without effective and transparent refund mechanisms), sales taxes, and customs duties. These instruments can raise money in the short run, but they do so by shaping the economy in unhelpful ways: penalizing scale, encouraging fragmentation, and rewarding concealment.

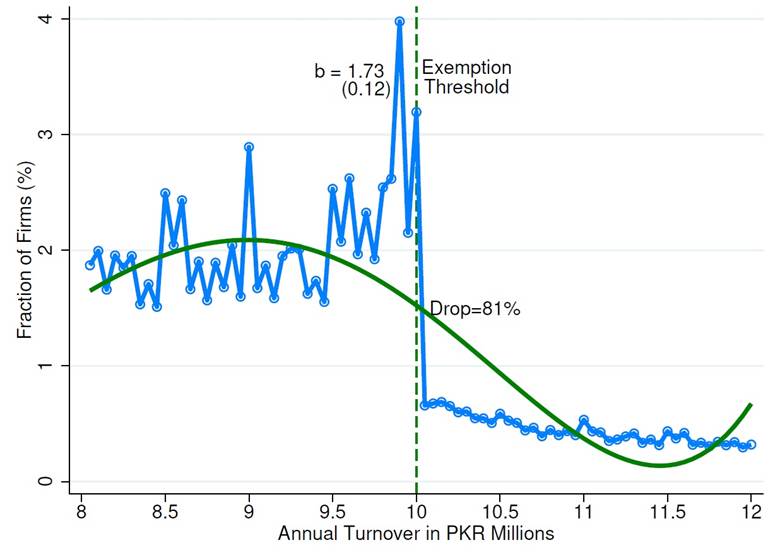

A vivid example comes from the VAT threshold: firms with turnover below PKR 10 million are exempt from VAT registration and remittance. The predictable result is bunching firms cluster just below the threshold, not only through misreporting but also by limiting growth or splitting into smaller entities.

Figure 5: A tax notch that discourages growth: bunching below the VAT threshold. When a firm grows, the tax system punishes it; unsurprisingly, firms choose not to grow. Source: Bashir et al. (2024)

Turnover taxation offers another illustration. In Pakistan’s minimum-tax regime, turnover taxes are layered alongside profit taxes precisely because they are harder to evade. But they come at a price: turnover taxes account for 50–60% of firms’ tax liabilities and contribute 60–75% of corporate tax revenue, while distorting production and discouraging innovation. This is what low-capacity taxation looks like: the state extracts revenue where it can, not where it should. And then wonders why productivity stagnates.

The missing base is not small shops. It is protected sectors. If Pakistan wants meaningful revenue, it must confront sectors where money is large, records are manipulable, and political power is organized. Take wholesale and retail trade (WRT): it contributes over 18% of GDP yet accounts for less than 3% of direct tax collection. Real estate, too, is undertaxed; fragmented valuation systems and weak regulation encourage speculative investment and low productive capacity. Agriculture is the most politically delicate, and therefore the most instructive. Despite contributing nearly 20% of GDP, agriculture’s share in tax revenues is “negligible,” thanks to exemptions and weak enforcement. The point is not to squeeze subsistence farmers; it is to tax wealthy landlords and high-value intermediaries. In all three sectors, the problem is not the absence of policy ideas. Pakistan has never lacked reform proposals. The problem is that reforms often fail to diagnose behavior, power, and incentives before prescribing solutions.

The quiet scandal of tax expenditures

Pakistan’s tax code is also riddled with carve-outs—exemptions, preferential rates, and special treatments that are often justified as growth-promoting but operate as privilege-preserving. According to the FBR’s Tax Expenditure Report 2024, federal tax expenditures amounted to 54.15% of the FBR’s total tax collection in FY 2022–23. Many are implemented via SROs, a practice that corrodes transparency and deepens perceptions of elite capture. The damage is not only fiscal. Exemptions skew investment—toward real estate speculation, away from productive activity—and they weaken compliance by making the system appear negotiable.

Equity: when a tax system taxes consumption and subsidizes inequality

Because direct taxation of high earners and high-value sectors is politically hard and administratively weak, Pakistan leans on indirect taxes. These are regressive by construction: they tax what people spend, not what they can afford. The consequence shows up in international comparisons. Pakistan ranks 62nd out of 66 countries in tax progressivity in the CEQ Institute’s assessment. What makes this particularly corrosive is that regressivity is paired with distrust. Tax evasion is widely normalized; paying taxes can be seen as naïve; citizens believe that revenues will not translate into public benefits. The social contract frays from both ends.

A way out: treat tax reform as applied science

Pakistan’s tax debate tends to swing between moral exhortation (“people must comply”) and technical tinkering (“digitize everything”). Neither is enough. Digitization without diagnosis can automate dysfunction. Compliance campaigns without credibility can produce more “junk filers.” The alternative is a scientific approach: data-driven, behaviorally informed, and rigorously evaluated before being scaled. This is not a call for endless pilot projects; it is a call for discipline—stop scaling what has not been shown to work. The roadmap is straightforward:

1) Strengthen data infrastructure—and use technology with humility

Modernize and integrate datasets across federal and provincial authorities for real-time collection and analysis. But crucially, technology must be piloted and evaluated against specific problems: identifying evasion patterns, optimizing enforcement, and streamlining processes.

2) Build in-house analytics and evaluation capacity

Tax authorities need dedicated units that can do analytics, behavioral design, and policy evaluation—testing interventions through RCTs or quasi-experiments (consumer lotteries, targeted enforcement, taxpayer engagement) before scaling.

3) Partner with researchers—and grow a local research ecosystem

Share anonymized data (with privacy safeguards), fund targeted studies, and build sustained collaborations with universities and think tanks so reforms are grounded in local realities.

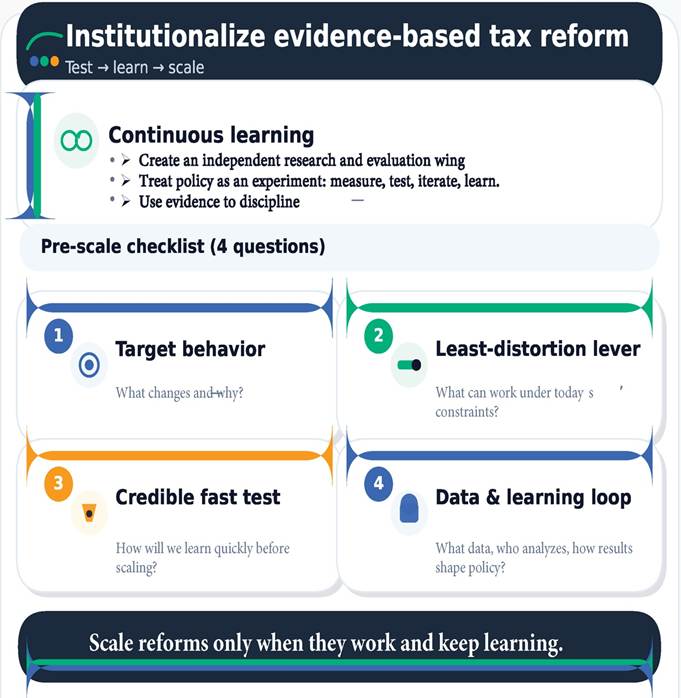

4) Institutionalize evidence-based policymaking and continuous learning

Create an independent research and evaluation wing (for example, within the Ministry of Finance) to assess reforms, build feedback loops, and keep policy adaptive as the economy evolves.

This is not managerial fashion. It is what serious states do when they confront complex systems: they measure, test, iterate, and learn. Pakistan’s history shows that “intent and effort are not enough”; what has been missing is a framework that disciplines political urgency with evidence.

Four questions every tax reform should answer before it is scaled

- What behavior are we trying to change—and why is it happening now?

- What is the least distortionary lever that can plausibly work under current capacity?

- How will we test impact credibly (and quickly) before expansion?

- What data will be produced, who will analyze it, and how will learning be institutionalized?

Figure 6: Institutionalizing evidence-based tax reform: continuous learning and a pre-scale checklist to test, learn, and scale responsibly.

The political economy of realism

A scientific approach does not evade politics; it confronts it more intelligently. Some reforms fail not because the economics are wrong but because the politics are ignored. Others “succeed” on paper by producing activity (registrations, filings, portals) rather than outcomes (revenue, fairness, growth). Pakistan has had too many of both.

If the state wants citizens to pay, it must first show that payment buys something more than paperwork. Evidence from Punjab suggests this is possible: when citizens receive valued public services and see a link between taxes and services, willingness to pay property tax increases. Trust, like revenue, is not demanded; it is earned.

Pakistan’s tax problem is solvable. But it will not be solved by expanding the register of the powerless, nor by layering new distortions on old weaknesses. It will be solved by doing what Pakistan’s tax system has rarely done: focusing enforcement where the money is, designing policy around behavior, and treating reforms as hypotheses to be tested—not slogans to be announced.

That is what a capable tax state looks like. And it is the only kind of state that can afford development.

References

Bashir, Muhammad, Zehra Farooq, Usama Jamal, and Mazhar Waseem. 2024. “Size-Based Policies and Firm Growth: Evidence from Pakistan.” Working Paper

Farooq, Zehra, Obeid U. Rehman, and Mazhar Waseem. 2024. “Predistribution vs. Redistribution: The Role of Taxes, Transfers, and Public Spending in Reducing Inequality,” Working Paper.

Federal Board of Revenue. 2024. Tax Expenditure Report. https://download1.fbr.gov.pk/Docs/2024791472531156TaxExpenditureReport202409.07.2024.pdf

Lustig, Nora, ed. 2023. Commitment to Equity Handbook: Estimating the Impact of Fiscal Policy on Inequality and Poverty. Brookings Institution Press.

Ministry of Finance. 2024. “Fiscal Development.” In Pakistan Economic Survey 2023-24. Government of Pakistan. https://www.finance.gov.pk/survey_2024.html